Menu

Florida & Texas Hurricane Damage Claims Attorney — Fighting for Full Compensation

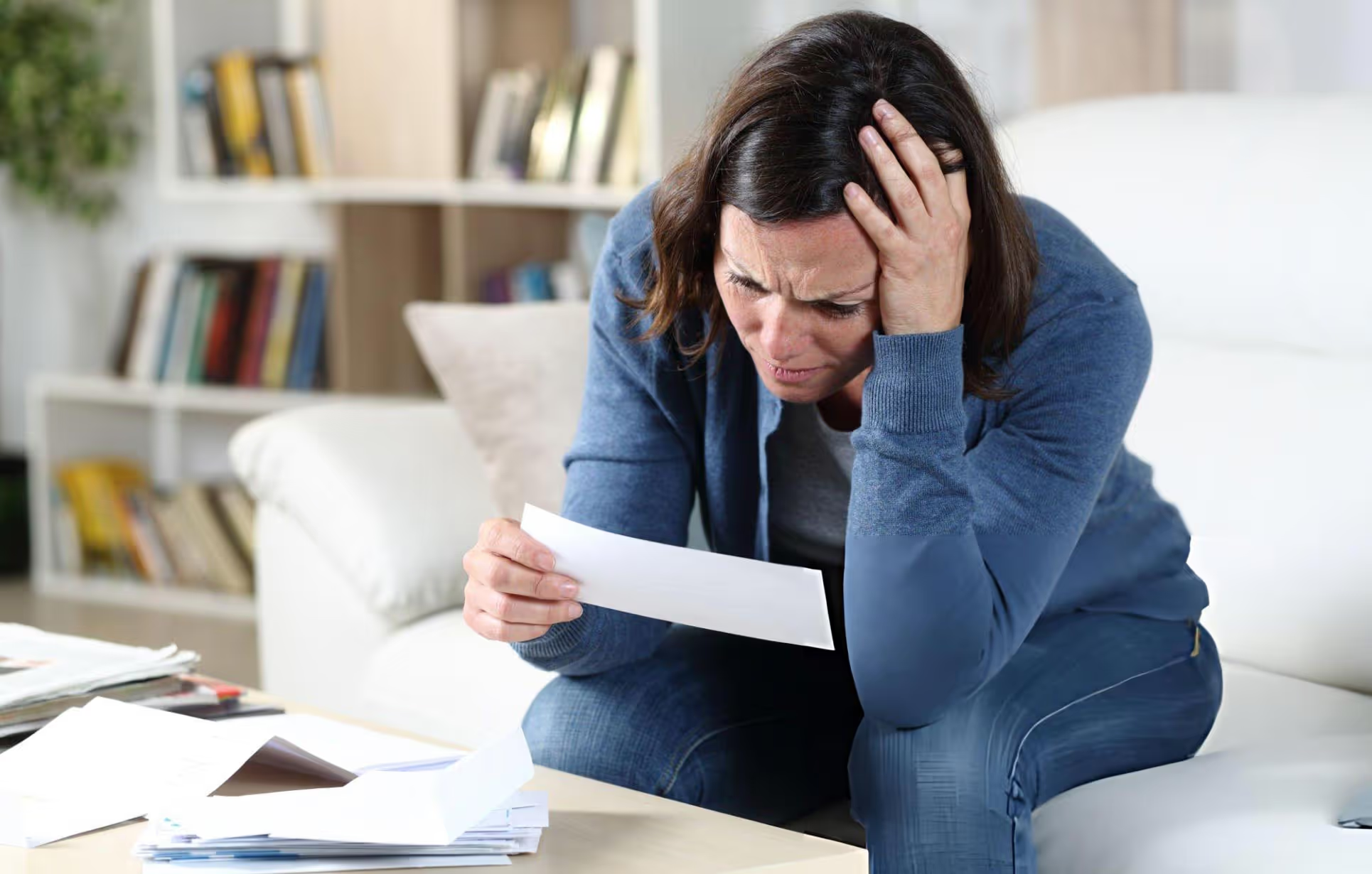

When your insurer delays, underpays, or denies your hurricane insurance claim, Finman Law Group's experienced hurricane damage attorneys go to work — at no upfront cost.

Experienced Hurricane Damage Attorneys Serving Florida & Texas

Hurricanes are a part of life in Florida and Texas — but the destruction left in the aftermath of a hurricane can change a family or business forever. Roofs ripped apart, windows blown out, water pouring into walls and ceilings, mold spreading within days, electrical systems destroyed, and entire structures compromised.

After a hurricane strikes, you expect your homeowner's insurance to help you rebuild. Instead, many property owners face delays, underpayments, or denials of their legitimate claims at the moment they need help the most.

At Finman Law Group, our hurricane damage claim lawyers fight aggressively to make sure your insurance company pays what your policy promises. Hurricane property damage claims are some of the most complex and heavily disputed claims in the insurance industry — and we know exactly how to challenge every tactic insurers use to avoid paying.

If your insurance company has denied your claim, underpaid you, or misrepresented your coverage, contact us today for a free case evaluation. You pay nothing unless we win.

Understanding Florida & Texas Hurricane Damage Insurance Claims

What Damage Is Caused by a Hurricane?

Hurricane damage is rarely limited to one part of a property. High winds, flying debris, wind-driven rain, storm surge, and pressure changes can cause widespread destruction across your home or business.

Common types of damage caused by a hurricane include:

- roof damage, missing shingles or tiles, and full structural failure

- broken windows and doors

- water intrusion and ceiling or wall damage

- electrical system damage

- mold growth from moisture left untreated

- damage to HVAC systems

- fences, sheds, and exterior structures

- business interruption losses

- and flooding, depending on your policy terms

Insurance companies often try to separate these damages to reduce payouts. Our damage attorneys make sure they evaluate the full scope of the loss — including hidden and secondary damage.

Why Insurers Deny or Underpay Hurricane Insurance Claims

Hurricane claims are among the most expensive claims insurers face. To protect their profits, insurance companies use predictable tactics to minimize what they pay on a claim for hurricane damage.

Common Insurance Company Excuses

Insurers routinely cite reasons such as "no storm-created opening," "wear and tear," "old roof," "pre-existing damage," "wind-driven rain not covered," "damage caused by flood, not wind," "cosmetic damage only," "insufficient evidence of wind damage," and "improper maintenance."

These excuses are designed to save the insurer money — not to protect you. Every insurance policy contains specific language that insurers use to deny or limit claims. Our hurricane damage attorneys know how to review your insurance policy, interpret the policy terms in your favor, and challenge every one of these tactics.

If your insurance company has denied your claim, our experienced attorneys can help you file a supplemental claim, reopen the dispute, or pursue bad faith damages if the insurer acted unfairly.

Wind vs. Flood: The Most Common Hurricane Coverage Dispute

After a hurricane makes landfall in Florida or Texas, insurers often blame damage on flooding instead of wind — because flood damage is typically covered under a separate flood insurance policy. This is one of the most common and most frustrating disputes hurricane damage claim lawyers handle.

Wind damage is usually covered under your homeowners' insurance policy and includes roof damage and structural damage, broken windows and doors, wind-driven rain entering through a storm-created opening, exterior damage from flying debris, and additional damage caused by wind-related pressure changes.

Flood damage, by contrast, requires a separate flood insurance policy and covers rising water and storm surge, groundwater intrusion, and water entering from the ground up.

Insurance adjusters frequently misclassify wind-related damage as flood damage to avoid paying under your primary policy. Our damage claim lawyers know how to prove the true cause of loss and hold your insurance provider accountable.

Review your insurance policy carefully — or let us review it for you. Many homeowners don't know what hurricane coverage they have until after a hurricane strikes.

Florida & Texas Hurricane Claim Laws Protect You

Both Florida and Texas require insurance companies to investigate hurricane property damage claims promptly, pay undisputed amounts quickly, evaluate all storm damage including hidden and secondary losses, follow building code requirements in every repair, and provide written explanations for any denial or reduction.

If your insurer fails to meet these obligations, they may be acting in bad faith. Finman Law Group uses state insurance law to hold insurers accountable and, where applicable, pursue additional bad faith damages on your behalf.

How Hurricane Damage Spreads Through Your Property

Hurricane damage rarely stays limited to the roof or exterior. Wind-driven rain can enter through roof openings, cracked shingles, damaged tiles, broken windows, gaps in doors, soffit and fascia damage, and attic vents. Left unaddressed, this leads to water intrusion, mold growth, electrical hazards, structural weakening, ceiling collapse, warped flooring, and damaged insulation.

Insurance adjusters often ignore this hidden and secondary damage to reduce the payout on your claim. Our experienced hurricane damage attorneys work with roofing experts, engineers, water mitigation specialists, mold assessors, contractors, and public adjusters to document every dollar of loss the insurer overlooked.

How Our Hurricane Damage Claim Lawyers Fight for You

When you hire Finman Law Group, our experienced attorneys take over the entire claim process and build a strong case for full compensation.

We Review Your Insurance Policy

Every insurance policy contains unique terms, exclusions, and coverage limits. We review your insurance policy line by line to identify every dollar of coverage you may be entitled to — including coverage you may not know you have.

We Conduct a Full Property Assessment

We work with roofing experts, engineers, water mitigation specialists, mold assessors, contractors, HVAC specialists, and public adjusters to document every area of damage the insurer ignored or undervalued.

We Challenge Lowball Estimates

Insurers often use outdated pricing and incomplete scopes of work. Our damage attorneys demand accurate, full-cost estimates that reflect what your repairs actually require.

We Demand Full Repairs — Not Patchwork

Hurricane damage often requires full roof replacement, window and door replacement, drywall and insulation replacement, flooring replacement, electrical repairs, and mold remediation. We make sure the insurer pays for what is necessary, not what is cheapest for them.

We Enforce Building Code Requirements

Florida and Texas require repairs to meet current building codes. Insurers must pay for necessary code upgrades. We make sure they do.

We File Supplemental Claims

If the insurer missed or undervalued damage, a lawyer can help you reopen the claim and file a supplemental claim for the additional damage.

We Pursue Bad Faith Damages

If your insurance company has denied your claim unfairly, delayed without reason, or acted in bad faith, they may owe you additional compensation beyond the original claim value.

We Litigate When Necessary

If the insurer refuses to pay what your policy promises, we take them to court. Our damage attorneys have a track record of success in hurricane damage litigation across Florida and Texas.

What To Do After a Hurricane Strikes

- First, document everything. Take photos and videos of all storm damage immediately — before any cleanup or repairs begin.

- Second, protect your property. Tarp the roof, board windows, and take reasonable steps to prevent additional damage. Your insurance policy may require this.

- Third, do not throw away damaged materials. Damaged property is evidence. Keep it until your attorney advises otherwise.

- Fourth, contact your insurance company. Notify your insurer promptly. Delays in reporting can affect the claim process.

- Fifth, request a full copy of your policy. Review your insurance policy — or have an attorney review it for you. You may have hurricane coverage you are not aware of.

- Sixth, do not accept the first offer. The first settlement offer from an insurer is almost always too low. Consult a hurricane damage attorney before you sign anything.

Finally, call Finman Law Group at (786) 786-9633. We take over communication with the insurer immediately and begin building your claim for full compensation.

Houston Hurricane Damage Claims & Texas Property Insurance

Finman Law Group handles hurricane damage insurance claims throughout Texas, including the greater Houston area. Houston hurricane events have left thousands of homeowners and businesses fighting for fair insurance coverage. Our experienced damage attorneys understand Texas property insurance law and the specific challenges that come with hurricane claims in the region.

Whether your hurricane coverage dispute involves wind damage, flood insurance, roof claims, or a denied claim, our damage claim lawyers are ready to help you recover the full value of your loss.

Frequently Asked Questions About Hurricane Damage Insurance Claims

Does homeowners' insurance cover hurricane damage?

Yes — most homeowner's insurance policies cover wind damage caused by a hurricane. However, insurers often dispute the cause of loss, misclassify damage, or apply exclusions to deny or reduce your claim. An experienced hurricane damage attorney can help you fight back.

What is a hurricane deductible?

A hurricane deductible is a separate, higher deductible that applies specifically to hurricane-related damage. In Florida, hurricane deductibles are typically a percentage of your home's insured value rather than a flat dollar amount. Understanding your hurricane deductible is an important part of the claim process — and our attorneys can help you interpret the policy terms that apply to your situation.

Does insurance cover wind-driven rain?

Often yes. If wind created an opening and rain entered through that opening, it is generally considered wind damage and covered under your primary property insurance policy. However, this is one of the most commonly disputed issues after a hurricane makes landfall in Florida or Texas.

Do I need a separate flood insurance policy?

Standard homeowners' insurance policies do not cover flooding from rising water or storm surge. If your property was flooded, a separate flood insurance policy, typically through the National Flood Insurance Program, is required to cover that damage. Our attorneys can help you navigate claims under both your primary policy and any separate flood insurance policy.

Can I reopen a hurricane claim?

Yes. If your insurer underpaid or missed damage, you may be able to file a supplemental claim for the additional damage, even after your original hurricane claim has been closed. Contact us today to find out if your claim can be reopened.

My insurance claim is denied — what do I do?

If your claim is denied, do not accept that decision as final. A hurricane damage attorney can review your insurance policy, identify the basis for the denial, and challenge it. If your insurance company has denied your claim without a valid reason, they may be acting in bad faith and owe you additional compensation.

Do I pay anything upfront?

No. We offer a free case evaluation, and you pay nothing unless we win.

Why Choose Finman Law Group as Your Hurricane Damage Attorney

Our experienced hurricane damage attorneys bring a track record of success representing homeowners and businesses in Florida and Texas. We have deep knowledge of hurricane coverage disputes, including wind vs. flood conflicts, bad faith insurance practices, and underpaid claims. We understand Florida and Texas insurance law and know how to use it to your advantage. There are no upfront fees and you pay nothing unless we win. We provide full support from the initial review of your insurance policy through litigation if necessary, and every new client receives a free case evaluation with no obligation.

Rebuild With Strength. Rebuild With Support.

If you have suffered hurricane property damage and your insurer is not paying what you are owed, Finman Law Group's experienced hurricane damage claim lawyers are ready to fight for you.

Call (786) 786-9633 today or contact us for a free case evaluation. You pay nothing unless we win.

-web.avif)

Contact Form

Fill out the form below to get in touch with our team.