Topic:

Property & Casualty

Article content

Your deductible is one of the most important numbers in your policy, and also one of the most misunderstood as well. Here's what every Florida homeowner should be aware of before filing a claim.

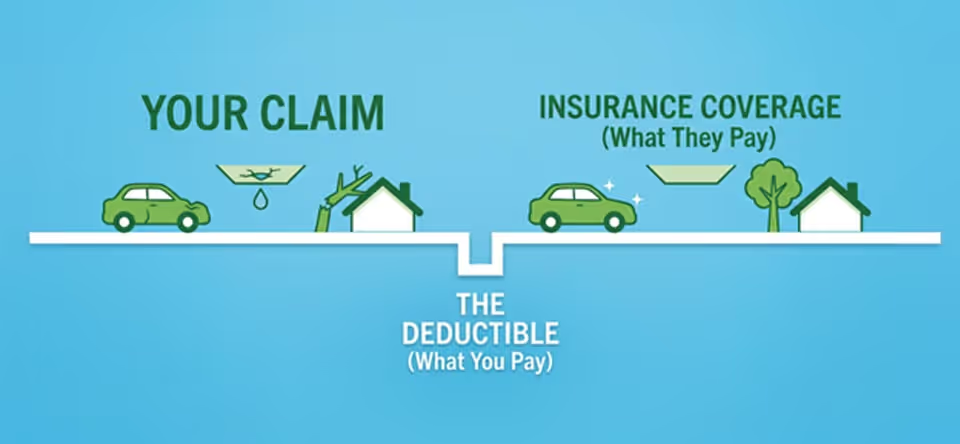

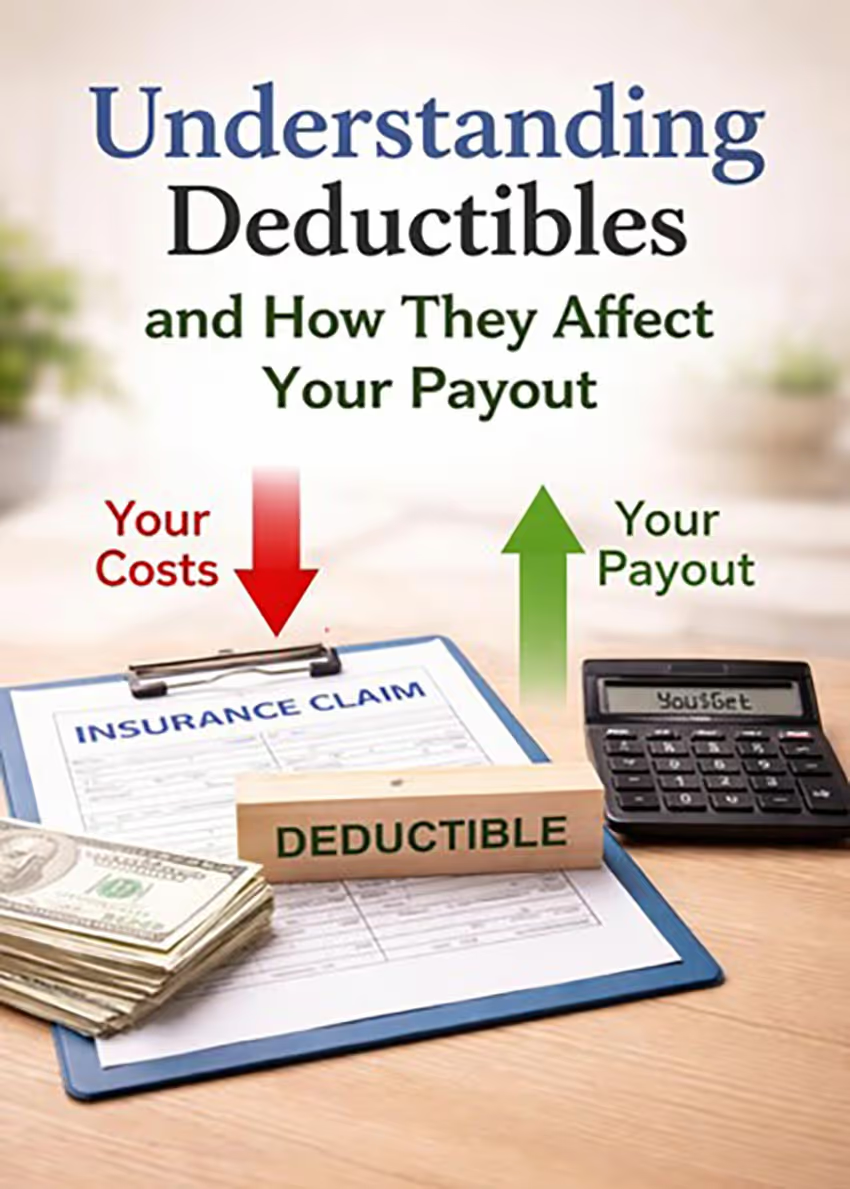

A deductible is the portion of a covered loss that comes out of your pocket before your insurance company pays anything. Think of it as your share of the risk. It is the amount you agree to absorb so that your insurer covers the rest.

On paper, it's straightforward: if a storm causes $15,000 in damage and your deductible is $3,000, your insurer owes you $12,000. But that clean math assumes your insurer applies the deductible correctly, calculates the loss accurately, and doesn't reduce your payout through depreciation or disputed scope. In practice, any one of those assumptions can fall apart.

Florida can make this more complicated than most states due to heightened weather activity. Between hurricanes, tropical storms, wind events, and routine flooding, there are more scenarios where deductibles come into play, and thus, more ways they can be applied in manners that may not favor you.

Most homeowners assume they have a single deductible. In Florida, your policy may include up to three — each of which is typically triggered by different causes of loss, and each calculated differently.

Hurricane Deductible: This is the one most Florida homeowners underestimate. Unlike a flat dollar amount, it's calculated as a percentage of your home's insured value, typically 2% to 5%, and only applies when damage is caused by an officially declared named hurricane. On a home insured for $400,000 at a 2% rate, you're responsible for the first $8,000 out of pocket. At 5%, that's $20,000 before your insurer contributes a dollar.

All-Peril Deductible: This is the fixed dollar amount most people are familiar with. It covers the majority of losses outside of hurricanes or named storms — fire, theft, burst pipes, and similar events. It is more predictable, but disputes arise when an insurer reclassifies a loss as wind-related, bumping it into a more expensive category.

Windstorm Deductible: Some Florida policies include a standalone deductible for wind damage from events that aren't officially named hurricanes. These can include severe thunderstorms, tropical storms, or straight-line winds. This creates a gray area insurers sometimes exploit, applying a higher windstorm deductible when a homeowner expected the standard flat rate to apply.

Say a storm causes $12,000 in damage to your roof and interior. Your policy has a $5,000 deductible. Your insurer's maximum payout is $7,000 — and that's the ceiling, not a guarantee. Insurers can still reduce the payout through depreciation, disputes over scope of damage, or other adjustments buried in the fine print. The check that arrives may be far less than what your repairs actually cost.

Insurance companies don't always apply deductibles the way you would expect. A common scenario in Florida is that a homeowner assumes the flat all-peril deductible applies — only for the insurer to argue that wind was involved, triggering the much higher windstorm or hurricane deductible instead. That reclassification alone can cost thousands.

Florida law governs how and when certain deductibles can be applied. If your insurer is using a deductible that doesn't match your policy language, or doesn't align with Florida statutes, that's something worth challenging with the right legal help.

Pull out your declarations page and identify every deductible listed, not just the main one. Look specifically for "hurricane," "windstorm," or "named storm" language. Then compare how your claim was handled against what the policy actually says. If the numbers don't add up properly, that's a red flag worth investigating. Document everything along the way, including contractor estimates, adjuster reports, and all communications with your insurer. That paper trail is essential if you need to dispute a decision.

We know how insurers work and we know how to push back. If your claim felt underpaid, or your deductible was applied in a way that didn't seem right, let's take a look at it together. There's no cost to talk.

Contact Finman Law Group today at (786) 786-9633 for a free consultation!

Learn how Florida daycare injury claims work, steps parents should take after an accident, and how to hold negligent childcare facilities accountable now.

Discover how windstorms impact Florida homeowners. Learn about damage prevention, insurance claims, and protecting your investment with expert guidance.

Explore cruise injury laws for Florida travelers. Learn about maritime rules, legal steps, and protecting your rights when accidents occur on ocean voyages.